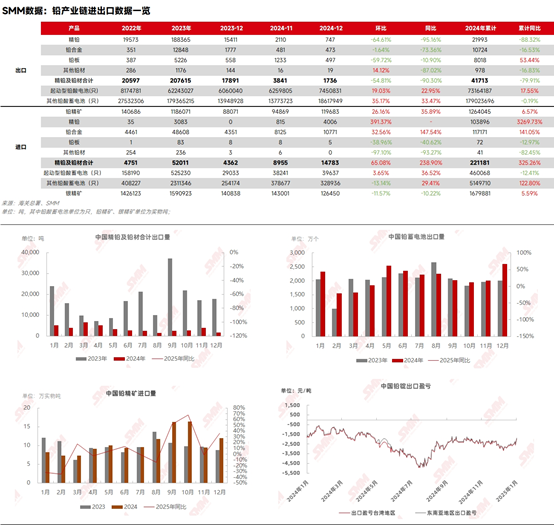

According to customs data, imports of lead concentrates in December 2024 reached 119,700 mt, up 26.16% MoM and 35.89% YoY. Cumulative imports of lead concentrates in 2024 totaled 1.264 million mt in metal content, up 6.57% YoY. The main import sources of lead concentrates in December were Russia, Australia, and Peru, with the total imports from these three countries accounting for 44.5%.

Compared with 2023, newly commissioned lead and zinc mines in 2024 gradually ramped up production, easing the supply deficit of lead concentrates in H2. Additionally, the opening of the import window mid-year boosted trade volumes of imported ores.

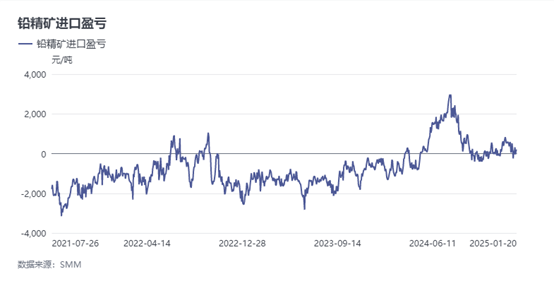

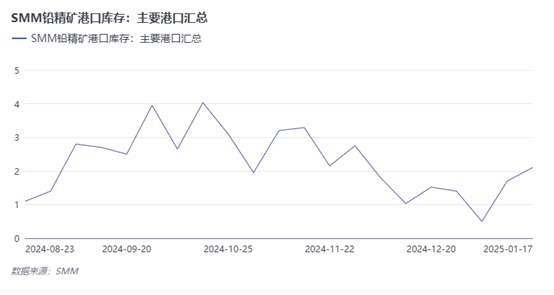

Recently, in terms of import profit and loss for lead concentrates, lead prices showed LME outperforms SHFE, and the theoretical import profit and loss of lead concentrates remained in a slight profit state. Entering January, new orders for 2025 began execution, and inventories of lead concentrates at main ports continued to increase. January imports of lead concentrates are expected to remain flat or increase slightly compared to December. However, after domestic smelters completed concentrated procurement for stockpiling, transaction quotations decreased. With the Chinese New Year holiday approaching, February arrivals of lead concentrate orders may face delays. Although the supply deficit of lead concentrates in Q1 2025 is expected to ease compared to Q1 2024, smelters remain pessimistic about a short-term rebound in pb60TC quotations.